CHICAGO — Rising commodity costs affected Conagra Brands’ performance during the third quarter of fiscal 2018, ended Feb. 25. The challenge facing company management is determining if the inflationary pressure is a long-term trend or will ease as the year progresses.

“…Inflation is trending well above the 2.7% we anticipated as part of our initial fiscal ‘18 guidance,” said Sean M. Connolly, president and chief executive officer, during a conference call with financial analysts on March 22. “The inflation impacts both input costs and transportation costs, which have risen sharply across the industry. The net result in Q3 was that despite our actions to price ahead of our categories, gross margins were pressured.

“As we’ve said before, margins may move around quarter-to-quarter beyond our normal seasonality. And as we continue through our transformation, we will look to exit lower-margin businesses and enhance our portfolio with margin-accretive innovation and acquisitions quarter-to-quarter.”

Conagra’s net income during the third quarter totaled $362.8 million, equal to 91c per share on the common stock, and an increase compared with the same period of the previous year when net income equaled $179.7 million, equal to 42c per share.

Sales for the quarter ticked up less than 1% to $1,994.5 million from $1,981.2 million the year prior.

The dramatic increase in net income is attributable to the federal tax legislation passed in December, favorable selling, general and administrative expenses as well as favorable advertising and promotion expenses compared to the same period of the previous year.

Conagra’s gross profit fell 3.6% during the quarter to $599 million.

“… Gross profit was impacted by several factors this quarter, including our intentional choices on how to invest in the top line,” said David S. Marberger, chief financial officer. “We continued to focus our brand building activity on above-the-line marketing investments with retailers and we reduced A&P investments. This impacted gross margin. We also saw challenges on the cost side. Our core productivity programs continued to deliver, but their benefits were more than offset by significant input cost inflation in the quarter, including transportation.”

Mr. Connolly said he did not expect cost inflation to impact Conagra’s long-term margin outlook.

“ … Some of these transitory factors we’re dealing with right now, we don’t expect them to have an impact on our longer-term margin outlook,” he said. “But obviously, kind of the topic of the moment right now in our industry is inflation, productivity, pricing.

“Obviously, inflation happens. It is a fact of life and we view it as our job to navigate it as effectively as we possibly can to protect our margins. Productivity and pricing are two critical levers and we’ve got strong capabilities around each of those levers. That doesn’t mean that there won’t be short-term volatility, particularly when you’re in a window where commodity inflation pivots from being benign to being acute …”

“Obviously, inflation happens. It is a fact of life and we view it as our job to navigate it as effectively as we possibly can to protect our margins. Productivity and pricing are two critical levers and we’ve got strong capabilities around each of those levers. That doesn’t mean that there won’t be short-term volatility, particularly when you’re in a window where commodity inflation pivots from being benign to being acute …”

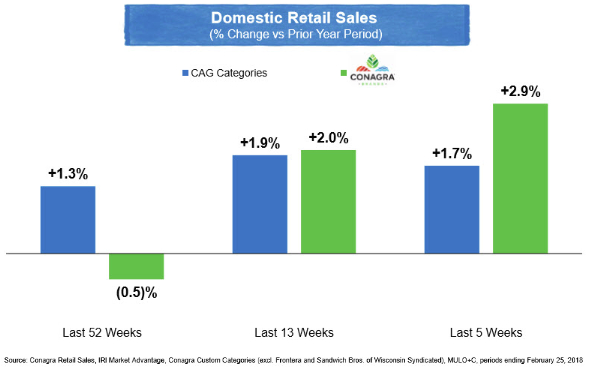

In the company’s largest business unit, Grocery & Snacks, sales fell 1% to $838 million during the quarter. Consumption trends continued to improve in the quarter, and non-promoted consumption exceeded expectations, according to the company. Volume declined 4%, driven by retailer inventory reductions, which were higher than anticipated, and deliberate actions to optimize distribution on certain lower-margin products.

“… We expected this segment’s sales to be down in Q3, given the impact of the hurricanes in Q2,” Mr. Connolly said. “Although it’s certainly early days, we’re pleased with the underlying consumption trends in our Grocery & Snacks portfolio, which bodes well for this segment’s long-term, top line growth prospects.

“We expect to accelerate from here with a particular focus on snacking. We’re energizing our snacking playbook with ramped up innovation, a focus on driving impulse consumption, marketing with a purpose and better price pack architecture.”

Sales in Conagra’s Refrigerated & Frozen business unit ticked up 3% to $689 million during the quarter. Organic net sales grew 3% behind volume growth of 2% driven by core business improvements and innovation launches in the Marie Callender’s, Healthy Choice, and Banquet businesses, the company said.

Sales in Conagra’s Refrigerated & Frozen business unit ticked up 3% to $689 million during the quarter. Organic net sales grew 3% behind volume growth of 2% driven by core business improvements and innovation launches in the Marie Callender’s, Healthy Choice, and Banquet businesses, the company said.

“Frozen retail sales have improved materially,” Mr. Connolly said. “Frozen consumption was up nicely again in the quarter, continuing a strong trend in the domain. And we think we have a lot of room to go from here as our distribution performance continues to improve and dollar sales growth has followed.

“Taking a step back, one of the things we’re most determined about in frozen is that, given our strong performance, we have ample room to capture our fair share of shelf space and grow organically. We expect this to be a tailwind for our frozen business going forward as we gain our fair share of distribution. Progress we’ve made in frozen demonstrates that our plan is working and we're not resting on what we've accomplished to date.”

Mr. Marberger said Conagra expects its diluted earnings per share from continuing operations to be in the range of $2.03 to $2.05 for the year, up from the range of $1.95 to $2.02 management announced during its presentation at the Consumer Analyst Group of New York conference held in February in Boca Raton, Fla.